Financial Position and Forecasting of Boeing

In this report “Financial Position and Forecasting of Boeing” we discuss, The Boeing Company, founded in 1916, is a cornerstone of the global aerospace industry. With over 170,000 employees and operations in over 150 countries, Boeing is a major manufacturer of commercial jetliners, defence systems, and space technologies. Its business is structured across three core segments: Commercial Airplanes (BCA), Defence, Space & Security (BDS), and Global Services (BGS).

For decades, Boeing held a dominant position in its duopoly with Airbus. Still, a series of crises—most notably the 737 MAX safety failures, the COVID-19 pandemic, and recurring quality issues—have significantly eroded its financial and operational standing. In 2024 alone, Boeing reported an $11.8 billion net loss and a 14% drop in revenue to $66.5 billion, its worst performance since the height of the pandemic.

The purpose of this report is to critically analyse Boeing’s current financial position following a period of prolonged instability. This includes evaluating key financial indicators such as profitability, liquidity, solvency, and operational efficiency.

The report will examine Boeing’s financial statements from 2022 to 2024, benchmark its performance against Airbus and Lockheed Martin, and assess future outlook through forecasting and scenario planning. It will conclude with strategic recommendations aimed at restoring financial resilience and rebuilding long-term stakeholder trust.

Read more: Financial Decision Making of Central Asia Metals

Financial Position Analysis

Boeing Company’s financial position at the end of 2024 shows a company still under considerable stress, despite brief signs of recovery in the previous year. While there were some improvements in cash and liquidity, core financial indicators such as profitability, solvency, and operational efficiency point to continued weaknesses. The following analysis is based on Boeing’s most recent financial statements and industry benchmarks.

Table 1 Boeing Income Statement Highlights (2022–2024) (USD millions, except per-share)

| Year | 2022 | 2023 | 2024 |

| Total Revenues | $66,608 | $77,794 | $66,517 |

| Commercial Airplanes | $26,026 | $33,901 | $22,861 |

| Defense, Space & Sec. | $23,162 | $24,933 | $23,918 |

| Global Services | $17,611 | $19,127 | $19,954 |

| Operating Income | –$3,519 | –$773 | –$10,707 |

| Net Income | –$4,935 | –$2,222 | –$11,817 |

| Diluted EPS | –$8.30 | –$3.67 | –$18.36 |

Boeing’s profitability:

Boeing Company’s profitability has continued to deteriorate, reflecting operational inefficiencies, high costs, and quality issues. In 2024, the company posted a net loss of $11.8 billion, a dramatic decline from the $2.2 billion net loss in 2023 and a stark reversal of its partial recovery. This represents Boeing’s largest loss since 2020, extending a streak of five consecutive unprofitable years.

The Boeing company’s operating income also plunged from –$773 million in 2023 to –$10.7 billion in 2024, largely due to the prolonged labor strike, ongoing production flaws, and losses in both the Commercial Airplanes (BCA) and Defense (BDS) segments.

The impact on margins was severe. Boeing’s gross margin fell from +9.9% in 2023 to –3.0% in 2024, indicating that the cost of goods sold exceeded revenue, an alarming sign for a manufacturer of Boeing’s scale.

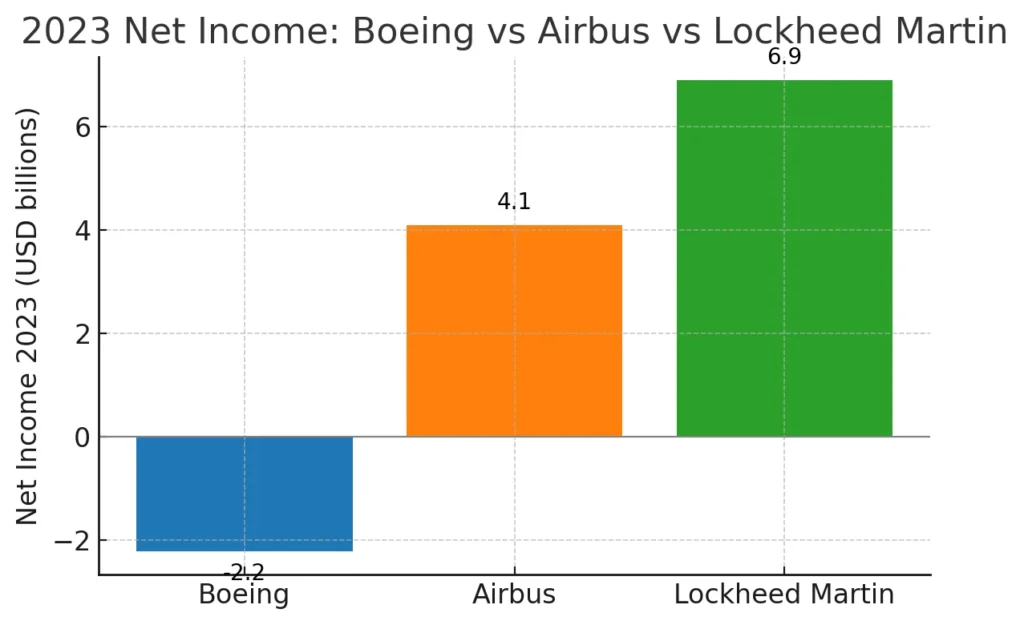

The net profit margin dropped to –17.8%, compared to –2.9% the year before. In contrast, competitors like Airbus and Lockheed Martin recorded positive margins of 5.8% and 10.2%, respectively, in 2023. This underlines Boeing’s ongoing inability to translate its revenues into profit.

Return on assets (ROA) has also been negative for two consecutive years. It stood at approximately –1.6% in 2023 and worsened to –7.6% in 2024, with net income far below the scale of Boeing’s expanding asset base. Return on equity (ROE) is not meaningful due to negative shareholders’ equity, which was –$17.2 billion in 2023 and –$3.9 billion in 2024.

Even if calculated, the resulting positive figure (due to the negative denominator) would be misleading. A breakdown using the DuPont method highlights the core issue: Boeing’s low asset turnover and persistently negative profit margins, rather than insufficient leverage, are the primary culprits for poor ROE.

Liquidity:

Despite its profitability challenges, Boeing’s short-term liquidity position saw marginal improvement in 2024. The current ratio increased from 1.14 in 2023 to 1.32 in 2024, reflecting $128 billion in current assets against $97 billion in current liabilities.

On the surface, this indicates adequate liquidity. However, more than $60 billion of current liabilities are customer advance payments—liabilities that don’t require near-term cash outlays but still represent significant delivery obligations. Stripping these out reveals stronger underlying liquidity.

Boeing Company’s quick ratio, which excludes inventory, also improved slightly from ~0.18 in 2023 to 0.28 in 2024. This is based on ~$37.5 billion in liquid assets (cash, short-term investments, and receivables) against $97 billion in liabilities.

However, this still reflects a reliance on converting large inventories into cash. Boeing ended 2024 with $26.3 billion in cash and short-term investments, which provides a temporary buffer, but sustained negative cash flow would erode this cushion quickly.

Boeing’s solvency:

Boeing Company’s solvency remains a significant concern. The company’s debt load stood at $53.9 billion at the end of 2024, almost unchanged from $52.3 billion in 2023. While Boeing executed a major equity and preferred stock issuance in late 2024, raising $15.8 billion in common stock and $4.9 billion in convertible preferred, its overall capital structure remains fragile.

Due to negative equity, traditional debt-to-equity ratios are not meaningful. Instead, Boeing’s debt-to-assets ratio was around 34.5% in 2024.

More critically, interest coverage ratios have collapsed. In 2023, EBIT could only cover –0.31× of interest expenses, and by 2024, this had worsened to –3.93×, reflecting EBIT of –$10.7 billion against roughly $2.7 billion in annual interest expense.

While Boeing Company covered interest in 2023 using operating cash flow (positive $5.96 billion), it posted –$12.1 billion in operating cash flow in 2024, marking a major regression. The Altman Z-score for Boeing in 2024 was estimated below 1.0, placing it in the “distress zone”, which typically indicates a high risk of bankruptcy. Although Boeing’s strategic importance may reduce real default risk, its financial indicators reflect severe solvency issues.

Efficiency:

Operational efficiency has also declined. Boeing’s asset turnover dropped from 0.57× in 2023 to 0.43× in 2024, as total assets grew (to $156 billion) and revenues fell. Inventory turnover worsened as well. With $57.4 billion in cost of goods sold and $87.6 billion in inventory, the 2024 inventory turnover ratio was just 0.66×, meaning inventory sat for approximately 1.5 years on average—a highly inefficient figure for a manufacturer. In 2023, this ratio was only slightly better at 0.75×.

The buildup in inventory reflects both undelivered jets and rework due to production issues, locking up capital that should be generating revenue. Boeing’s receivables turnover remains healthy due to the nature of its contracts (customers pay in advance or on delivery), and accounts payable are also in line with standard supplier terms. However, until Boeing can improve delivery rates and reduce work-in-progress inventory, its efficiency will remain under pressure.

Strengths and Weaknesses

Boeing Company remains a strategically significant player in the aerospace sector, but its financial profile reveals a mixed picture of potential and vulnerability. A closer look at its financial and operational data highlights both notable strengths and pressing weaknesses.

Strengths:

One of Boeing Company’s core strengths is its scale and market position. It operates in a global duopoly alongside Airbus, maintaining a significant share of the large aircraft market, with annual revenues ranging between $66 and $78 billion from 2022 to 2024. Its $554 billion order backlog, representing more than 8,600 aircraft, ensures future revenue streams and underlines strong demand from airlines and governments.

Boeing’s Global Services (BGS) segment also provides stable, high-margin income—approximately $19 billion annually—by supporting the installed fleet through maintenance and aftermarket services. In 2023, Boeing generated $4.4 billion in free cash flow, showing its potential to recover when operations run smoothly. The company also raised $20 billion in new equity and preferred stock in 2024, boosting its liquidity and confirming investor confidence in its long-term relevance.

Weaknesses:

However, Boeing’s weaknesses are severe and systemic. Most critically, it has posted five consecutive years of net losses, including –$11.8 billion in 2024 alone. Its profitability remains far below peers—Airbus had an EBIT margin of 8.2%, while Boeing’s dropped to –1% in 2023 and –16.1% in 2024.

The Boeing company also carries a $54 billion debt burden, while its Altman Z-score fell below 1.0 in 2024, signalling high bankruptcy risk. Cash flow is volatile, swinging from +$4.4B in 2023 to –$14.3B in 2024, largely due to inventory build-up and production delays.

Frequent manufacturing flaws, program overruns, and certification delays—for example, with the 737 MAX and 777X—continue to erode efficiency and inflate costs. These issues, unless addressed, pose a direct threat to Boeing’s ability to deliver on its backlog and regain financial stability.

Benchmarking

A comparison between Boeing and its key competitors—Airbus and Lockheed Martin—reveals Boeing’s major underperformance in profitability, solvency, and efficiency, despite having a similar revenue scale.

In terms of revenue, Boeing reported $77.8 billion in 2023, ahead of Airbus’s $70.8 billion (converted) and Lockheed Martin’s $67.6 billion. However, Boeing’s sales were unstable, falling 14% in 2024, whereas Airbus maintained 11% year-on-year growth and delivered 735 aircraft compared to Boeing’s 528.

Profitability is a major concern for Boeing. Its net margin was –2.9% in 2023 and –17.8% in 2024, while Airbus posted 5.8% and 6.1%, and Lockheed achieved 10.2%. Boeing’s operating margin was also significantly lower (~–1%) versus Airbus’s 7.6% and Lockheed’s 12%. Boeing’s Return on Equity (ROE) was negative due to its negative equity, whereas Airbus reported an ROE of ~19%, and Lockheed’s exceeded 100% (though inflated by buybacks).

Boeing Company also lags in efficiency. Its asset turnover ratio (~0.5) was lower than Airbus’s (~0.52) and much lower than Lockheed’s (~1.3). Its inventory turnover, at 0.7×, compares poorly to Airbus’s 1.8×, showing Boeing ties up more capital in undelivered aircraft.

On solvency, Boeing’s financial risk is far higher. With over $54 billion in debt and negative equity, its Altman Z-score fell below 1.0, placing it in the “distress” zone. In contrast, Airbus and Lockheed have strong balance sheets, healthy interest coverage, and better credit ratings.

Financial Forecast and Recommendations (2025–2026)

Boeing’s financial future hinges on its ability to stabilize production, reduce costs, and rebuild stakeholder confidence. Based on current trends and analyst expectations, Boeing’s base-case revenue is projected to reach approximately $85 billion in 2025, rising to $95 billion in 2026.

Net income could return to ~$2 billion in 2025 and potentially rise to $6–7 billion in 2026, assuming delivery volumes reach 650 and 750 aircraft, respectively, and operating margins improve to 6–10%. Free cash flow (FCF) is expected to recover to $2 billion in 2025 and $5–6 billion by 2026, though this remains below Boeing’s historical performance targets.

To support this recovery, Boeing must urgently implement aggressive cost control strategies. A key issue remains the excessive cost of rework and inefficiencies in production, which drove the –3% gross margin in 2024. By focusing on Lean manufacturing, automation, and quality assurance (including training over 100,000 staff in 2023), Boeing Company could realistically restore gross margins to 15% by 2026. Further savings should be sought by renegotiating contracts with key suppliers like Spirit AeroSystems, ideally ahead of Boeing’s planned acquisition.

Second, Boeing Company needs to reduce its debt burden, which stood at $53.9 billion in 2024, while equity remained negative. We recommend targeting $10 billion in debt repayment by 2026, funded from improved FCF, to reduce annual interest expense and improve solvency.

This deleveraging would help lift Boeing’s Altman Z-score, currently below 1.0, out of the financial “distress zone.”

Third, Boeing Company must continue investing in quality control and R&D, not just to meet regulatory expectations, but to restore confidence in its engineering. R&D spending, at $3.8 billion in 2024, should be maintained or strategically increased to support future aircraft development and sustainability initiatives like SAF and hybrid propulsion. This aligns with long-term value creation and addresses customer concerns.

Finally, rebuilding brand and stakeholder trust is vital. Boeing Company must consistently deliver on promises, maintain transparency with regulators and investors, and uphold safety as a core value. By prioritizing stakeholder alignment, particularly with employees, customers, and suppliers, Boeing can gradually recover its reputation and pricing power.

Conclusion: Financial Position and Forecasting of Boeing

This report has critically examined Boeing’s financial position and strategic outlook. The analysis reveals a company with significant structural challenges: persistent losses, high leverage, weak profitability, and operational inefficiencies.

Despite posting revenue of $77.8 billion in 2023, Boeing’s net margins remained negative, and its financial health deteriorated further in 2024 with a staggering net loss of $11.8 billion. In contrast, peers like Airbus and Lockheed Martin continue to outperform Boeing in profitability, efficiency, and financial stability.

Yet, Boeing’s core strengths—its $554 billion backlog, global duopoly position, and robust services segment—provide a foundation for recovery. Financial forecasts suggest that, with disciplined execution, Boeing can return to profitability by 2025 and generate up to $5–6 billion in free cash flow by 2026.

The recommendations in this report “Financial Position and Forecasting of Boeing”—cost control, debt reduction, investment in quality and R&D, and rebuilding stakeholder trust—are essential not just for survival, but for Boeing to regain its competitive edge.

Addressing its internal inefficiencies and restoring confidence across the value chain will be key to improving profitability, liquidity, and long-term resilience. Boeing’s future depends not just on delivering planes, but on delivering credibility—financially, operationally, and ethically.